Mitt Romney’s now-infamous statement, “My job is not to worry about those people,” pretty much sums up the Republican nominee’s true feelings about who he represents. And if you’re in serious debt, it looks like he’s talking about you too.

If you are among the 22.4 million people who owe college debt, a record 20 percent of all American households, Romney makes clear that he represents big student loan companies, not you. If you are one of the 55.4 million households with credit card debt, the 77.7 million households, or the million people who lost their homes to foreclosure in the first half of 2012, Romney doesn’t worry about you, either. (After all, this is the guy whose answer to the foreclosure crisis is to do nothing, and just “Let it run its course and hit the bottom.”)

With the help of our Democratic leaders, the country is taking its first tenuous steps toward building a more transparent, truthful, equal, efficient and cheaper credit system, where the fee-happy mortgage chicanery that caused our current economic malaise is unambiguously illegal.

Candidate Romney promises that if elected president he would do everything in his substantial power to tear down that nascent system, returning us all to the Wild West-style laissez-faire practices that got us into trouble in the first place.

Here are five ways in which Romney would be devastating for everyday Americans.

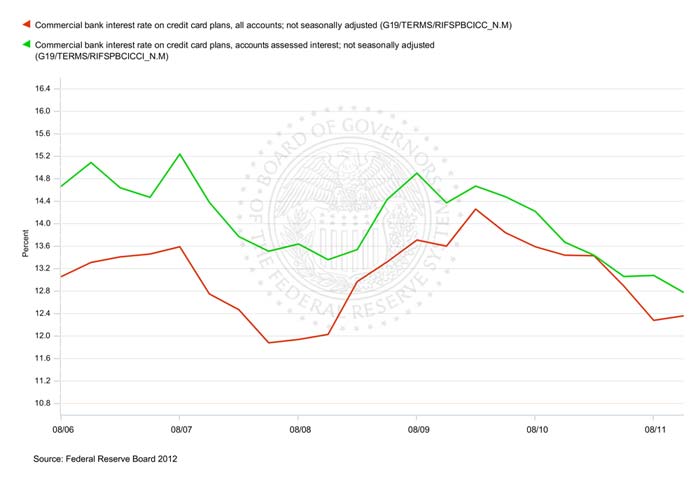

1. Credit Cards Will Become More Expensive and Deceptive.

For more than a year, Romney has been carping about the supposed harm caused by the Credit Card Accountability Responsibility and Disclosure (CARD) Act, which passed with support of such diehard big bank apologists as (wait for me now) Mitch McConnell and Jim DeMint. Romney says the CARD act, “produced federal restrictions on credit card companies that have already led to higher interest rates, higher annual fees, and lower credit limits, especially for middle-class borrowers.”

He’s completely wrong. Interest rates and fees actually dropped immediately after the CARD Act took effect, according to the Federal Reserve. The reason is obvious: The CARD Act is doing a great job of protecting consumers from all kinds of abuses, including deceptive pricing schemes. Among its many features, the act prohibits raising rates on existing credit balances except in three very specific circumstances; requires credit card issuers to give cardholders 45 days’ notice before increasing interest rates; forbids the types of billing and payment shenanigans issuers once used to hike rates and reap exorbitant fees; limits issuers from charging more than one overdraft fee per month; forces issuers to gain cardholders’ explicit consent before signing them up for costly overdraft protection; and requires credit card companies to disclose to consumers how long it will take to pay off their balance by making only the monthly minimum payment. . (Even this great law is a work in progress and has its problems, including loopholes that allow issuers to charge new, higher rates sooner and more often than advertised, as Credit.com covered here.)

If you have a credit card (or two, or three, or four), you’re benefitting from these reforms right now. But hey, Mitt Romney ain’t worried about you. He wants to gut this legislation based on his “pro-consumer automatically means anti-business” worldview. If he succeeds, banks will be allowed to regress to the good old days when they could increase fees and interest rates whenever they felt like it, manipulate your bill’s due date to grab overdraft fees and no doubt worse.

2. Predatory Mortgages Will Return

Romney hates the Dodd-Frank Wall Street Reform Act even more than he does the CARD Act (but less than the Affordable Health Care Act). Forget tweaking the law; he wants to get rid of it entirely.

“I’d like to repeal Dodd-Frank,” Romney said. “The extent of regulation in the banking industry has become extraordinarily burdensome following Dodd-Frank.”

If he succeeded, that would include the Mortgage Reform and Anti-Predatory Lending Act, which does many good things, including banning the old kickback system in which lenders paid bonuses to mortgage originators who hoodwinked homebuyers into paying higher interest rates. This law requires lenders to ensure that borrowers can actually afford a mortgage, making it more difficult for lenders to trick homebuyers into loans that are either inappropriate to their economic standing or costlier than advertised simply to reap the origination fees, a practice that helped cause the mortgage boom and bust. It bars lenders from forcing homeowners into bogus, industry-controlled arbitration programs (rather than seeking redress in the courts), and in a number of cases prevents lenders from charging pre-payment penalties when homeowners manage to pay their mortgages off early.

These reforms are vitally important, not just for homeowners, but also for honest lenders and the economy at large. They reaffirm the American notion that our economic system should be based on real work and real value, not on deception and trickery.

3. Student Loans Will Be More Expensive.

Under the old system of higher education funding, the federal government used private lenders to dole out billions of dollars in student loans every year. The result was massive waste in the form of government subsidies to guarantee repayment or reimburse private companies when graduates deferred payment due to financial hardship, says Mitchell Weiss, a frequent Credit.com contributor and an expert on student loans.

In 2010, President Obama changed all that. By removing the private middlemen and making the Department of Education responsible for government loans, he saved taxpayers millions every year. He also pushed for and won legislation that caps graduates’ monthly loan payments at 10 percent of their incomes, gives borrowers more power to reduce their payments if their income drops, and gives them the opportunity to reduce or eliminate debt entirely if they commit themselves to careers that promote the public good. (For great background on all this, check out this summary by the New America Foundation, a nonpartisan think tank.)

Surprise! Romney wants to scrap all that. He proposes to get private lenders back into the lucrative game of government student lending, even though doing so would cost taxpayers and students billions extra in the form of subsidies and increased fees and interest charges, according to the Federal Education Budget Project..

What does Romney want struggling students to do instead? His considered plan: students should “shop around” for cheaper colleges.

That’s not a plan, it’s a downright insult.

4. Death to the CFPB.

The true target of the Romney “corporations are people” crowd is the Consumer Financial Protection Bureau, which he called “the most powerful and unaccountable bureaucracy in the history of our nation.”

Wrong again! Far from being some unaccountable attack dog, the CFPB is the only regulator of the financial industry whose decisions can be vetoed by other agencies. What’s more important is that in his quest to carry Wall Street’s sweat buckets and destroy the Bureau, Romney is willing to sacrifice the millions of hardworking Americans who just want a fair deal.

In its first year of existence, the Bureau already has proposed simple, easy-to-read disclosure forms that clearly explain in just one or two pages all the costs involved in a mortgage agreement or a credit card contract. That’s a huge improvement over current contracts, which sometimes prattle on for scores of pages and bury loads of hidden fees deep in the fine print.

If he succeeds in killing the CFPB, Romney’s Wall Street friends win. They get to keep loading us down with sneaky fees. And tens of millions of people with mortgages and credit cards lose.

5. More Exploitation by Payday Lenders and Debt Collectors

Anyone who’s ever run across these industries already knows what’s wrong. Payday lenders charge astronomically high interest rates, often between 400-700 percent, trapping low- and moderate-income families into a cycle of debt from which some might never escape. Every week seems to bring another scandal in which a debt collection company is caught illegally threatening consumers with jail time; revealing details about debts to neighbors and employers; and simply making up the paperwork required to prove in court that the consumer in question actually owes any debt at all.

It’s obvious that consumers need more transparency, education and protection from these deceptive practices, not less. Romney’s plan to kill the CFPB would stop those reforms after conception but before birth. Millions of vulnerable Americans will lose.

If you are ready for a president who believes that trickle-down economics is the answer to the problem of what to do in a global economy, and if you want the solution to look like an economic killing field where most of the country’s citizens are sacrificed on the altar of corporate greed of the very worst stripe, then by all means Mitt’s your guy..

Of course, I could be wrong. He could make things even worse.

Originally posted at the Huffington Post.

{kind=link}